Short-Term vs. Long-Term Crypto Capital Gains: What's the Difference?

How your holding period can dramatically impact your tax bill—and what you can do about it.

CAPITAL GAINS

Introduction

You've made a profitable trade—congratulations! But before you start planning how to spend your gains, there's an important question you need to answer: how long did you hold that cryptocurrency before selling?

The answer to that simple question can significantly impact how much tax you'll owe. The IRS divides capital gains into two distinct categories based on holding period, and the difference in tax rates can be substantial. Understanding this distinction is one of the most powerful tools in a crypto investor's tax planning toolkit.

This guide explains the difference between short-term and long-term capital gains, how they're taxed, and what strategies you can use to minimize your tax burden.

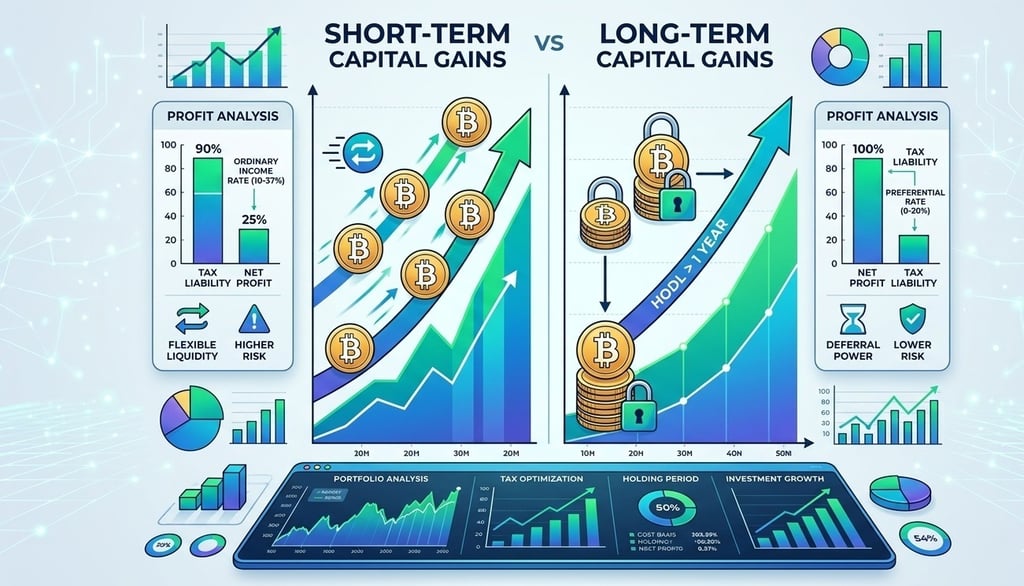

Short-Term Capital Gains: The Higher-Tax Bracket

Short-term capital gains apply when you sell or dispose of a cryptocurrency that you've held for one year or less.

The key characteristic of short-term gains is that they are taxed at the same rate as your ordinary income . This means they're added to your other income sources—like your salary, freelance earnings, or interest income—and taxed according to the regular income tax brackets.

For the 2025 tax year, ordinary income tax rates range from 10% to 37% , depending on your total taxable income and filing status . This means that if you're in a higher income bracket, your short-term crypto gains could be taxed at the maximum rate of 37%.

Example: Sarah buys Ethereum for $5,000 in January 2025. She sells it for $8,000 in November 2025, just ten months later. Because she held the asset for less than a year, her $3,000 profit is a short-term capital gain. If Sarah's ordinary income places her in the 24% tax bracket, she'll owe approximately $720 in taxes on this trade.

Long-Term Capital Gains: The Tax Advantage

Long-term capital gains apply when you hold a cryptocurrency for more than one year before selling or exchanging it.

The tax rates for long-term gains are significantly more favorable than ordinary income rates. For most taxpayers, long-term capital gains are taxed at:

0% for taxpayers in the lowest income brackets

15% for most middle-income investors

20% for high-income taxpayers

These rates have remained stable for 2025, with the 0% rate applying to single filers with taxable income up to $48,350 and married couples filing jointly up to $96,700 .

Example: Michael buys Bitcoin for $10,000 in January 2024. He sells it for $18,000 in February 2025, holding it for over a year. His $8,000 profit is a long-term capital gain. If Michael's income places him in the 15% long-term capital gains bracket, he'll owe approximately $1,200 in taxes—significantly less than if the gain had been short-term.

Why the Difference Matters

The gap between short-term and long-term rates can be dramatic. Consider this comparison for a hypothetical investor in the 32% ordinary income bracket:

Holding PeriodGainTax RateTax OwedShort-Term (11 months)$10,00032%$3,200Long-Term (13 months)$10,00015%$1,500

By waiting just two additional months to sell, this investor saves $1,700 in taxes—a 53% reduction in their tax liability. That's money that stays in their pocket rather than going to the IRS.

Real-World Example: Calculating Your Gain

Let's walk through a complete example to see how this works in practice.

The Scenario: You purchase 1 Bitcoin for $10,000 on March 15, 2024. You sell that same Bitcoin for $15,000 on April 20, 2025.

Step 1: Determine the holding period. From March 15, 2024, to April 20, 2025, is approximately 13 months. This qualifies as a long-term holding period (more than one year).

Step 2: Calculate the gain. $15,000 (sale price) - $10,000 (cost basis) = $5,000 capital gain.

Step 3: Apply the appropriate tax rate. Because this is a long-term gain, it will be taxed at the preferential long-term rates (0%, 15%, or 20%) based on your total taxable income for the year.

If this had been a short-term gain (sold within one year), the $5,000 would have been added to your ordinary income and taxed at your marginal rate—potentially as high as 37%.

Strategies to Optimize Your Holding Period

Understanding the tax implications of your holding period opens up several tax-saving strategies.

Strategy 1: The Long-Term Hold

The simplest strategy is to hold appreciating assets for more than one year whenever possible. If you believe in a project's long-term potential, waiting to sell can significantly reduce your tax burden. This is one reason the "HODL" mentality has genuine financial benefits beyond market speculation.

Strategy 2: Strategic Selling

Sometimes you need to sell before the one-year mark. In these cases, consider whether you have any losing positions that could be sold to generate capital losses, which can offset your short-term gains. This is known as tax loss harvesting.

Strategy 3: Year-End Planning

Review your portfolio toward the end of the calendar year. If you have gains in assets you've held for 11 months, it may be worth waiting a few more weeks to sell in the new year, pushing your holding period past the one-year threshold and converting a short-term gain into a long-term gain.

Strategy 4: Income Timing

If you have control over when you realize gains (for example, if you're a freelancer who can choose when to convert crypto payments to cash), consider realizing gains in years when your overall income is lower, potentially qualifying you for the 0% long-term capital gains rate.

Important Considerations

While the tax advantages of long-term holding are clear, there are some important nuances to keep in mind:

The holding period clock starts the day after you acquire the asset and ends on the day you sell it . This is a strict measurement, so be precise with your dates.

The one-year rule applies to each individual lot. If you bought Bitcoin on multiple dates, each purchase has its own holding period. When you sell, you can choose which specific lots to sell (if you've tracked them properly) to optimize your tax outcome.

Trading triggers a new holding period. If you trade one crypto for another, the clock resets on the new asset. The holding period for the new token begins on the day you receive it.

Gifted assets carry over the donor's holding period. If someone gives you crypto, your holding period includes the time the original owner held it .

The Bottom Line

The difference between short-term and long-term capital gains is one of the most impactful concepts in crypto taxation. By simply being aware of your holding periods and planning your sales strategically, you can potentially save thousands of dollars in taxes.

For new investors, the takeaway is clear: if you can afford to hold your appreciating assets for more than a year, the tax code rewards your patience with significantly lower rates. It's one of the few areas where doing less (trading less frequently) can lead to keeping more of your profits.

As always, every investor's situation is unique. Consulting with a tax professional can help you develop a personalized strategy that considers your specific income, goals, and portfolio composition.